Global Economics 6.10.25

Asia-Pacific

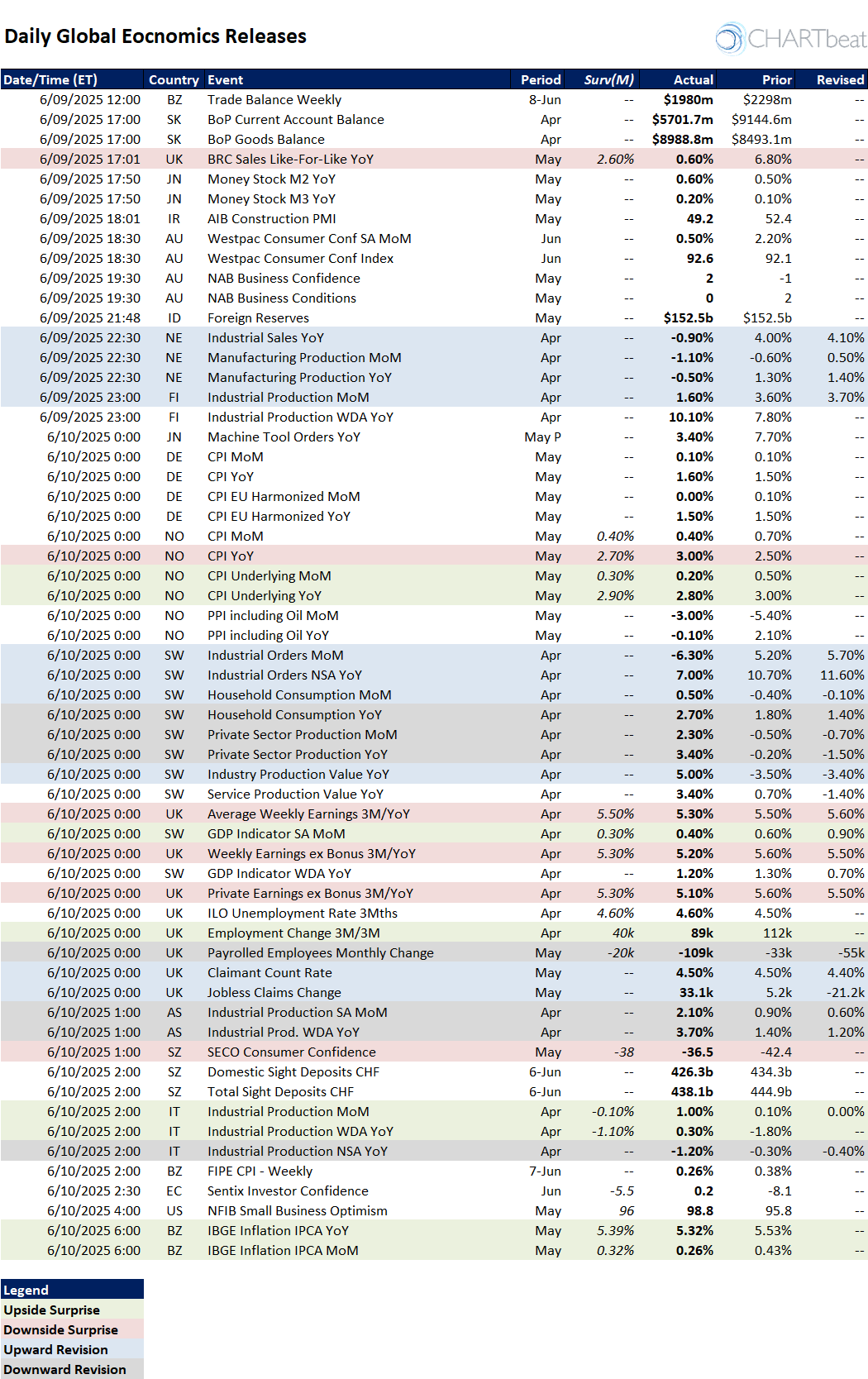

Japan

Japan's monetary and industrial data was generally steady but unremarkable. The monetary base grew slightly, with M2 at 0.6% YoY and M3 at 0.2%, both consistent with subdued monetary expansion. Machine Tool Orders decelerated to 3.4% YoY from 7.7%, indicating a potential softening in capital investment. Overall, there is no strong inflationary or growth pressure from these figures, suggesting a still-muted economic environment.

Australia

Australian data presented a mixed but mildly positive picture. Consumer sentiment, as measured by the Westpac Index, ticked up to 92.6, a marginal improvement from 92.1. However, the month-over-month momentum slowed to 0.5% from 2.2%. NAB Business Confidence improved to 2 from -1, indicating growing optimism among firms, although Business Conditions fell to 0 from 2. This divergence hints at a cautious outlook despite stabilized sentiment. Industrial production data for April showed resilience, with a MoM gain of 2.1% and a YoY increase of 3.7%, reflecting solid momentum in the real economy.

South Korea

The external sector showed weakness. The BoP current account balance narrowed sharply to $5.7B in April from $9.1B, reflecting a deterioration in secondary flows. Still, the goods surplus improved to $8.99B from $8.49B, suggesting export resilience but drag from services or income components.

Indonesia

Indonesia’s foreign reserves were steady in May at $152.5B, unchanged from the prior month. This signals ongoing external sector stability.

Europe

United Kingdom

UK data showed growing labor market softness. Employment change came in at 89k (below the prior 112k), while payrolled employees fell by a sharp 109k in May — a worsening trend from prior months. Jobless claims surged to 33.1k, and the claimant count rate held at 4.5%, but above the revised 4.4%. Despite this, wage growth remained elevated: average weekly earnings were up 5.3% YoY, and private sector earnings ex-bonus rose 5.1%, both showing some deceleration but still above inflation.

Retail activity was weak. BRC like-for-like retail sales grew only 0.6% YoY in May — well below expectations (2.6%) and a steep drop from April’s 6.8%, suggesting that consumer demand is fading quickly.

The ILO unemployment rate held at 4.6%, steady but up from earlier this year, indicating that the labor market is beginning to soften even if headline rates remain stable.

Germany

Inflation was tame. The national CPI for May was stable at 0.1% MoM and 1.6% YoY, while the EU harmonized readings were flat MoM and steady at 1.5% YoY. These numbers confirm that price pressures in Germany are largely contained.

Norway

Inflation data surprised to the upside. Headline CPI YoY rose to 3.0%, beating expectations (2.7%) and up from 2.5%. However, underlying CPI YoY cooled to 2.8% from 3.0%. MoM trends show a deceleration in underlying prices (0.2% vs. 0.3% expected). Producer prices contracted further: PPI MoM came in at -3.0%, and YoY at -0.1%, indicating broader disinflation in upstream costs.

Sweden

April data showed a clear rebound in production and consumption. Household consumption rose 0.5% MoM and accelerated to 2.7% YoY. Private sector production jumped 2.3% MoM and 3.4% YoY, swinging from prior contractions. Industrial production value surged 5.0% YoY from -3.5%, and services production rose 3.4% YoY from just 0.7%. However, industrial orders plunged 6.3% MoM, possibly foreshadowing a near-term pause in momentum.

GDP indicators showed mixed strength: SA MoM came in slightly above expectations at 0.4%, though down from 0.6%, and WDA YoY softened to 1.2% from a prior 1.3%.

Netherlands

Dutch manufacturing and industrial figures were notably weak. Manufacturing production declined -1.1% MoM and -0.5% YoY, and industrial sales dropped -0.9% YoY. These reversals from positive prior values point to a loss of momentum in April.

Finland

Finland's industrial output was solid. April industrial production rose 1.6% MoM, and the YoY rate surged to 10.1%, building on a previously strong 7.8%. This suggests a strong rebound in Finnish manufacturing activity.

Ireland

The AIB Construction PMI declined into contraction territory at 49.2, down from 52.4. This suggests that higher borrowing costs or weaker demand may be pressuring the construction sector.

Italy

Italy posted a notable upside surprise in April industrial production. MoM growth reached 1.0%, sharply beating the expected -0.1%. YoY WDA-adjusted production rose to 0.3%, reversing a prior -1.8% contraction. NSA YoY remained negative at -1.2%, but improved from -0.4%. Overall, this shows early signs of stabilization.

Switzerland

SECO Consumer Confidence improved to -36.5 in May, still deeply negative but better than -42.4. Meanwhile, sight deposits declined (CHF 426.3B domestic and CHF 438.1B total), possibly reflecting tighter monetary conditions or shifts in liquidity preferences.

Eurozone (Aggregate)

The Sentix Investor Confidence index sharply beat forecasts, rising to 0.2 in June from -8.1. This shift into positive territory suggests improving sentiment across the Eurozone, likely on the back of falling inflation and easing central bank rhetoric.

Americas

Brazil

Inflation continued to ease. The IPCA index rose 0.26% MoM in May, below both the forecast (0.32%) and April's 0.43%. On a YoY basis, inflation slowed to 5.32% from 5.53%. Weekly FIPE inflation also decelerated to 0.26% from 0.38%. These results confirm a cooling price environment that could support future rate cuts.

The trade balance for the week of June 8 came in at $1.98B, down from $2.3B the prior week, suggesting some softening in external trade flows.

United States

The NFIB Small Business Optimism Index rose to 98.8 in May, beating expectations (96) and improving from 95.8. This marks a meaningful uptick in small business sentiment and could signal better hiring and investment activity ahead, especially if inflation concerns continue to subside.