Global Economics 6.11.25

Asia

Japan

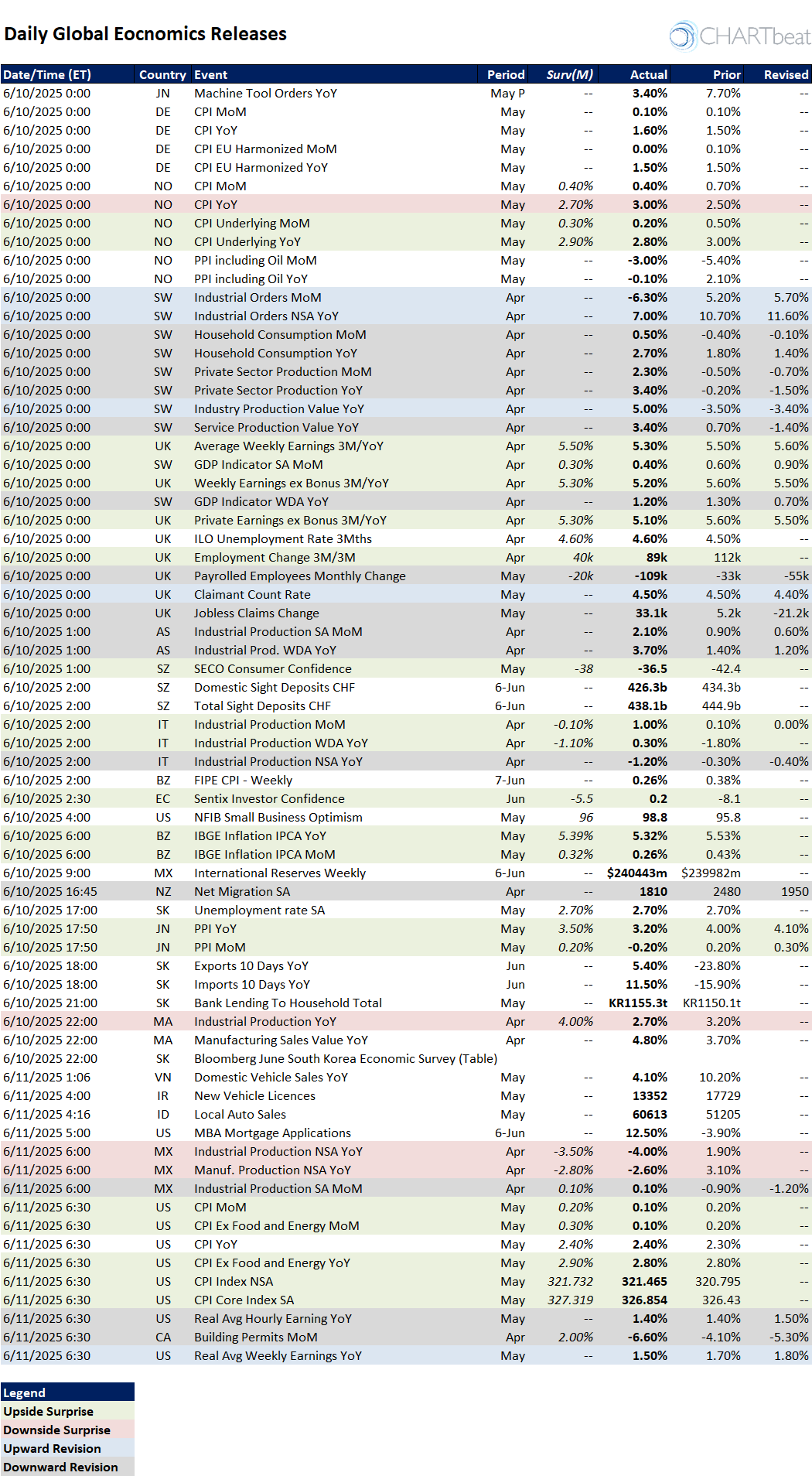

Japanese economic data shows continued weakness in industrial demand. Machine Tool Orders in May fell to 3.4% YoY from 7.7%, highlighting slowing capital investment. Additionally, PPI decelerated both monthly (-0.2% vs. 0.2% expected) and annually (3.2% vs. 3.5% expected), reinforcing disinflationary pressures at the producer level.

South Korea

South Korea's trade and financial data indicate a strong turnaround. 10-day exports rose sharply to 5.4% YoY from -23.8%, and imports surged 11.5%, reversing last month’s contraction of -15.9%. These figures suggest a potential rebound in global demand, particularly from China. Bank lending to households also increased, reaching KR1155.3 trillion, hinting at consumer credit growth.

Vietnam and Indonesia

Vietnam's domestic vehicle sales slumped to 4.1% YoY in May, sharply down from 10.2%, indicating cooling consumption. Conversely, Indonesia’s local auto sales jumped to 60,613 units, a healthy rise from 51,205, reflecting improving domestic demand conditions.

Taiwan

Taiwan’s industrial production rose 2.1% MoM and 3.7% YoY, suggesting strong momentum, likely supported by electronics and chip exports.

Europe

Germany

Inflation remained tame. CPI was unchanged MoM (0.1%) and the EU Harmonized CPI came in flat (0.0% MoM), pointing to subdued inflationary pressures and likely reinforcing the ECB’s dovish tilt.

Norway

Norwegian inflation surprised to the upside. Headline CPI YoY came in at 3.0%, above both expectations and the prior print (2.5%). However, underlying CPI fell MoM to 0.2% from 0.5%, indicating that core inflation may be softening. Meanwhile, PPI remains deeply negative (-3.0% MoM, -0.1% YoY), reinforcing disinflationary trends in upstream costs.

Sweden

Sweden posted a mixed bag. While industrial orders contracted sharply (-6.3% MoM), other indicators were robust: household consumption improved (0.5% MoM, 2.7% YoY) and private sector production rebounded (2.3% MoM, 3.4% YoY). GDP indicators remained modestly positive, suggesting resilient domestic demand.

Italy

Italy showed strength in industrial activity: Industrial Production MoM rose 1.0%, a significant beat over expectations (-0.1%) and prior. The YoY WDA figure also turned positive at 0.3%, reversing prior contractions, signaling a potential turning point in industrial output.

UK

UK labor market data was mixed. Wage growth slightly slowed across most metrics, and ILO unemployment held steady at 4.6%. However, the employment change surprised positively at 89k, beating the 40k forecast. That said, payrolled employees fell sharply by -109k, with jobless claims rising by 33.1k, indicating underlying labor market softening.

Switzerland

Consumer sentiment improved slightly, with SECO confidence at -36.5, up from -42.4, though still pessimistic. Sight deposits also fell, suggesting less liquidity in the banking system—possibly due to SNB balance sheet adjustments or capital outflows.

North America

United States

The U.S. inflation picture is mixed but generally cooling:

Headline CPI MoM rose just 0.1%, below the 0.2% forecast.

Core CPI MoM similarly underwhelmed at 0.1%, versus 0.3% expected.

YoY figures showed stability at 2.4% headline and 2.8% core.

These suggest that disinflation is gaining traction, which may prompt a more dovish Fed if sustained.

However, real earnings are declining:

Real Avg Weekly Earnings fell to 1.5% YoY from 1.7%.

Real Avg Hourly Earnings stagnated at 1.4% YoY.

On the business side, NFIB Small Business Optimism jumped to 98.8, signaling renewed confidence. Mortgage applications spiked 12.5%, likely in response to recent declines in yields.

Canada

Canadian housing permits dropped sharply (-6.6% MoM), a steep fall from the expected 2.0% gain, pointing to a housing slowdown amid higher rates and softer construction activity.

Mexico

Mexico’s industrial sector showed deterioration:

Industrial Production YoY came in at -4.0%, from 1.9% prior.

Manufacturing also contracted more than expected (-2.6% YoY).

While MoM data held steady at 0.1%, the YoY trends indicate deepening weakness in manufacturing output.Summary

Asia: Signs of recovery in South Korea and Taiwan offset weak vehicle sales in Vietnam and Japan’s soft inflation and industrial demand.

Europe: Mixed signals—Germany and Norway show inflation divergence, Italy and Sweden rebound in production, while the UK shows labor market fragility.

North America: U.S. inflation is softening, boosting market hopes for rate cuts, but earnings are stagnating. Canada and Mexico face industrial and construction headwinds.